Trade Transaction & Payment Services

Getting paid for international transactions, commonly known as Export Receivables, is very different from collecting payments from local companies due the extra documents and processes involved.

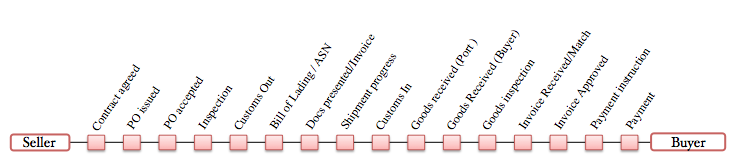

Key Documents and Processes in the Financial Supply Chain

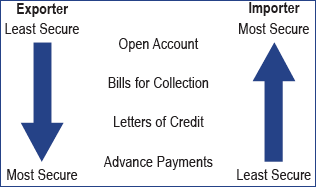

The main issue for the exporter/ the seller is not getting paid, whilst for the importer/the buyer it is the risk that the goods or services will not be delivered or will be damaged. Each of the trade payment systems has very different risks for the importer and the exporter as the figure below shows.

Trade Payment Systems

Source: SITPRO

Open Account

International trade has traditionally been carried out using Letters of Credit (LC) to fund and guarantee transactions. Over the last decade trade has been simplified by moving to Open Account based transactions in which the goods are shipped and delivered before payment is due, usually in 30-90 days. The buyer pays the supplier upon receipt of the goods with no backing other than the buyer's reputation. The large majority of trade is now by carried out by Open Account transactions.

This is the least secure method of trading for the exporter, but the most attractive to buyers. Goods are shipped and documents remitted directly to the buyer, with a request for payment on the agreed date. An exporter has little control of the process, except for imposing future trading terms and conditions on the buyer. The increased financial risk can be mitigated by costly credit insurance where needed. Not surprisingly over the last 2-3 years, due to the recent crisis, Letters Of Credit and traditional trade products have become slightly more popular again as companies are less sure of their trading partners, but the majority of trade is still carried out by Open Account.

Bills for Collection

In Bills for Collection transactions, the exporter's documentation is sent from their bank to the importer's bank. This occurs after shipment and contains specific instructions that must be obeyed. Should the buyer fail to comply, the exporter does, in certain circumstances, retain title to the goods, which may be recoverable. The buyer's bank will act on instructions provided by the exporter, via their own bank, and often provides a useful communication route through which disputes are resolved. The Bills for Collection process is governed by a set of rules, published by the International Chamber of Commerce (ICC), to which over 90% of the world's banks adhere. There are two types of Bill for Collection, which are usually determined by the payment terms agreed within a commercial contract: Documents against Payment (D/P) and Documents against Acceptance (D/A).

Bills for Collection are used in certain markets, particularly Asia, to fulfil Exchange Control Regulations. They are a cost-effective method of evidencing a transaction for buyers, where documents are handled (and reported) via the banking system.

Letters of Credit (L/Cs)

A Letter of Credit (also known as a Documentary Credit ) is a bank-to-bank commitment of payment in favour of an exporter (the Beneficiary), guaranteeing that payment will be made against certain documents that, on presentation, are found to be in compliance with terms set by the buyer (the Applicant). Like Bills for Collections, Letters of Credit are governed by a set of rules from the ICC specifying the terms and conditions. L/Cs are irrevocable and include detailed terms as part of the commercial contract. Letters of Credit, as well as including a bank's commitment to pay, also often include financing of the transaction and insurance cover.

Today L/Cs are often used where used where selling through the Open Account structure can be financially risky. A global techology company in particular markets use L/Cs to reduce the risk of non-payment without dampening sales to customers. There are several L/Cs service providers that will enable companies to operate L/Cs programmes without having to negotiate the complexities of L/C documentation and the changing rules and regulations.

Standby Letters of Credit (SBLCs) are similar to Bank Guarantees, sitting behind a transaction and are only called upon if the buyer fails to pay.

Advance Payment

Advance Payment is the most secure method of trading for exporters and, consequently the least attractive for buyers. Payment is expected by the exporter, in full, prior to goods being shipped.

Transaction Services

Many banks have developed individual web-based services to do process the international trade documents. There is also the multi-bank Trade Services Utility (TSU) from SWIFT which offers a common data platform using a simplified trade data set for matching this data from all banks.

Settlement / Payment Services

Most international trade settlement is carried out by SWIFT money transfer. There is still some use of banker's drafts but they are expensive and there is always the risk of the draft getting lost in transit.

The platforms focusing on SMEs typically offer payment by VISA and MasterCard and also by bank transfers.