Adoption of corporate real-time payments in the US: benefits and barriers

by Pushpendra Mehta, Executive Writer, CTMfile

Pushpendra Mehta, Executive Writer, CTMfile

On July 20, 2023, the US made a leap forward with the launch of FedNow, the US Federal Reserve's real-time payment service. FedNow is not the first instant payments service in the US. The Clearing House’s (TCH) real-time payments system, RTP®, has been live since November 2017.

The competition between RTP and FedNow is likely to intensify and will spur greater adoption of real-time payments in the US. In fact, as per the 2023 Real-time Payments Survey Report by the Association for Financial Professionals® (AFP), sponsored by TCH, 98% of organizations in the United States with “Annual revenue between $1 billion and $9.9 billion anticipate they will have adopted real-time payments within the next five years to send payments.”

The 2023 AFP® Real-time Payments Survey Report received responses from 310 treasury practitioners from organizations of varying sizes (under US$50 million to over $20 billion in annual revenue), representing a broad range of industries within the US.

Some of the key findings from the survey include the following:

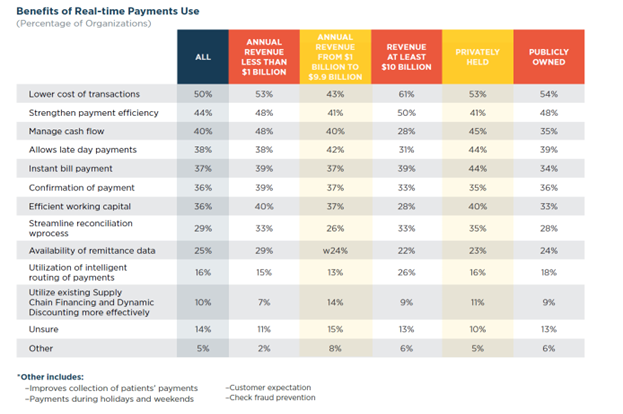

Recognized benefits of real-time payments

Over 60 percent of organizations with annual revenue of at least $10 billion observed that real-time payments (RTPs) lower the cost of transactions, aligning with the other AFP survey findings, where overall 50% of respondents stated that the primary benefit of using real-time payments is the reduction in transaction costs.

Source: 2023 AFP® Real-time Payments Survey Report

Strengthening payment efficiency was identified as the second most important benefit of adopting RTPs by 44% of survey respondents. Following closely, improved cash flow management was cited as the third most frequently recognized advantage of using RTPs. The fourth most often cited benefit is allowing late day payments, mentioned by 38% of respondents. Other pros of utilising real-time payments include:

— Instant bill payment (indicated by 37% of survey participants)

— Immediate confirmation of payment (36%)

— Enhanced working capital efficiency (36%)

— Streamlined payment reconciliation process (29%)

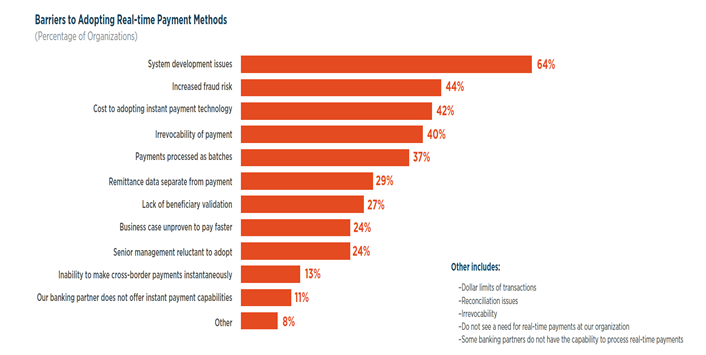

Barriers to adopting real-time payment methods

While RTPs offer various benefits to corporations, such as improved cash and liquidity management, there are some obstacles or barriers impeding the adoption of RTP methods.

Nearly two-thirds (64%) of survey participants identify system development issues as the main barrier hindering the implementation of RTPs within their organizations. According to the survey report, this is a matter of concern across the board, irrespective of the organization’s revenue size.

Source: 2023 AFP® Real-time Payments Survey Report

Given that RTPs are immediate and irreversible, there is less time to detect criminal activity or spot fraud. This makes RTPs more attractive to criminals, possibly explaining why an increased risk of fraud is a real concern and the second biggest barrier to adopting real-time payments, as expressed by 44% of the respondents.

The third significant barrier to embracing real-time payments is the cost of adopting instant payment technology, as mentioned by 42 percent of treasury respondents.

“IT resources have been a longstanding scarce resource when it comes to treasury and payments. It is often hard to move a project up to the top of the priority list for IT’s attention. This, coupled with the cost of system changes, makes the current business case for using real-time payments hard to justify”, the AFP survey explains.

The survey report further explains that “As time progresses, there is likely more throughput achieved in automated processes. Those companies who are finding the use case now are the trailblazers for those that will eventually make the system changes needed. As new enterprise resource planning (ERP)/treasury management system (TMS) software versions are rolled out, real-time payment connectivity through application programming interfaces (APIs) will likely be added in more and more, making the business case less of a hurdle from a cost standpoint if the technology is already in-house.”

The other two major roadblocks to the acceptance of real-time payment methods are irrevocability of payment (as stated by 40 percent of organizations) and payments processed as batches (pointed out by 37% of treasury executives polled).

The AFP survey delves deeper into why processing payments in batches is considered a limiting factor for the adoption of RTP methods. The survey notes “Organizations currently batch their payments as it is convenient and with the assistance of systems like intelligent payment routing, they are able to disseminate B2B transactions via various payment systems. Since real-time payments systems do not batch payments, this might be a barrier for those organizations where batch is a routine process.”

To conclude, despite the deterrents to integration of instant payments within organizations, the AFP survey estimates that by 2028, over three-fourths of entities expect to use RTPs for both sending and receiving payment transactions. This may be because the diverse benefits offered by real-time payments outweigh the hurdles in their adoption, which is why even though traditional payment methods continue to hold sway, forward-thinking enterprises are actively working towards embracing innovative digital payments technology, such as real-time payments.

Moreover, corporate treasury and finance leaders who integrate instant payments into their digital strategy will gain enhanced visibility into cash flow, enabling better cash and liquidity management. In doing so, they will also deepen ties with their suppliers, vendors, and customers, further improve the efficiency of working capital, and witness RTPs reshape the payments landscape for greater digital success.

Like this item? Get our Weekly Update newsletter. Subscribe today

About the author