Central Bank Digital Currencies are definitely coming but when?

by Jack Large

Digital currencies are here, e.g. Bitcoin, BUT the game changes when the Central banks get involved. Two recent events showed how seriously Central Banks are taking digital currencies.

BIS Working Paper No 880

This paper showed how central banks are working on/experimenting with digital currencies, as the map from the Working Paper 880 - “Rise of the central bank digital currencies: drivers, approaches and technologies” by Raphael Auer, Giulio Cornelli and Jon Frost - shows (see):

Source & Copyright©2020 – BIS

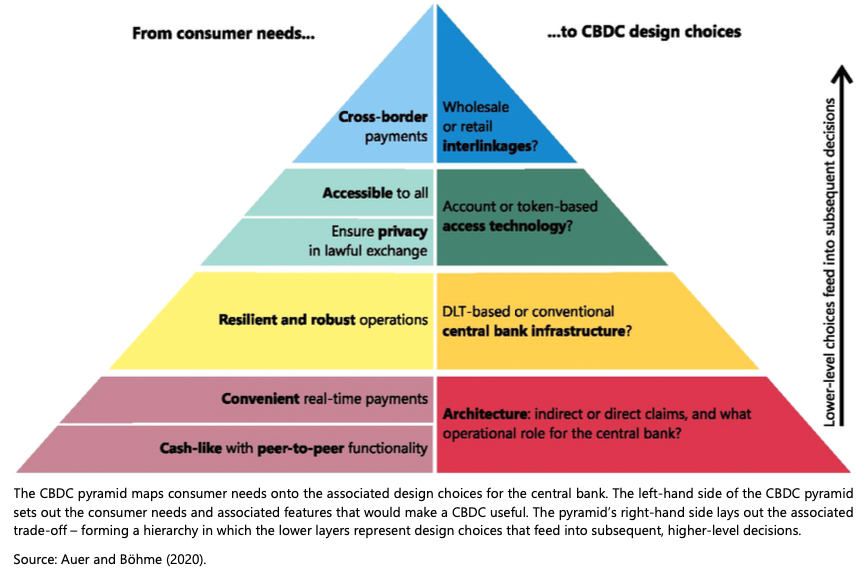

Main design choices

The authors classified the design approaches into a “CBDC Pyramid” for the consumer needs and the CBDC approaches:

Three prominent retail CBDC examples

The report then reviewed three prominent retail CBDC projects, namely the People’s Bank of China’s Digital Currency Electronic Payment (DC/EP) project; the Swedish Riksbank’s e-krona; and the work by the Bank of Canada on a CBDC as a contingency plan. The key conclusions from these projects were

- They are currently mainly within-country although there can be some international links via mobile phones.

- Multi-country solutions are being examined, e.g. “representatives of PBC noted that cross- country coordination can be useful to ensure consistent standards across borders”

- In Sweden, 1) the “CBDC would be intended as a complement to, not a replacement for cash” and 2) the costs of running such a system would be substantial

- In Canada, “The CBDC would not replace cash, but designed as a digital addition with advantageous resilience and accessibility features.”

Overall conclusions

This detailed analysis shows that central banks are taking CBDC’s seriously believing that:

- events such as the Covid-19 pandemic highlight the value of access to diverse means of payments, and the need for any payment method to be both inclusive and resilient against a broad range of threats

- central banks will continue to take a long-term view and carefully consider the role of CBDCs in a range of potential future scenarios.

CBDC used for e-commerce payments

Digital currencies are starting to be used in e-commerce. Finextra reported earlier this week that “Sygnum Bank's digital Swiss Franc (DCHF) was used to make a payment on the site of Swiss online retailer Galaxus. The transaction was enabled by Danish digital currency platform provider Coinify.”

And that “The value of Sygnum’s DCHF is pegged 1:1 to the Swiss Franc. When used for e-commerce payments, no intermediaries are involved and the transactions happen in real-time with stable values.”

As expected the benefits included:

- reduces costs for online retailers by eliminating card systems and protecting against fraud

- simplifying and speeding the customer purchase experience.

CTMfile take: Digital currencies will take payment systems/money back to its roots where value is exchanged between two parties, instantly and simply. This is clearly understood by the central banks who are getting involved as digital currencies could disrupt all payment systems as we know them today. But how are corporate treasuries going to cope with this new type of payment system?

Like this item? Get our Weekly Update newsletter. Subscribe today