Future is Open Banking, but will it really benefit corporate treasury departments?

by Kylene Casanova

The Euro Banking Association Open Banking Group - which is made up of bankers, payment service providers and consultants - has been studying, so called, Open Banking since 2016. Their latest report Open Banking: advancing customer-centricity focuses on how the latest technologies and thinking open up new ways of doing business for both the private and business customers.

Customer centricity evolution

The Executive Summary opens with these fine words, “ The power of putting customers at the centre of the corporate business strategy has been a well-known concept for decades. Many organisations across various industries have followed such a customer-centric approach to differentiate themselves and build a competitive advantage. However, in the digital era the customer-centric approach evolves to the next level, in particular, with regard to customers’ financial assets, personal data and digital service experiences and service options.” The report describes the move from customer centricity model 1.0 to 2.0 and the new dimensions and opportunities this brings.

Transition from a product-centric to a customer-centric approach

Source & Copyright©2017 - EBA

“Putting customers ‘in control’ can mean different things, essentially, it reflects a response to customer’s

desires to operate in an increasingly connected digital ecosystem. For the financial world, this can mean:

- Connect third party apps directly to a bank account and vice versa, e.g. for initiation of payments,

- Connect bank account data to apps, e.g. For financial planning and lending,

- Login (identification and authentication) at third party websites (public and private) with existing banking credentials,

- Share personal attributes, e.g. name, age, email address) with third party websites after authorisation with existing banking credentials.”

There is some discussion of how PSD2 is going to play a part in this revolution - each of the steps above is a revolution.

The report’s ‘use cases’ on connecting apps to multiple accounts, use on smart fridges and how to request a loans show the potential of Open Banking.

Open Banking as the basis for customer control

The report grapples with the issue of who is in control with Open Banking by identifying the three key dimensions of Open Banking:

Source & Copyright©2017 - EBA

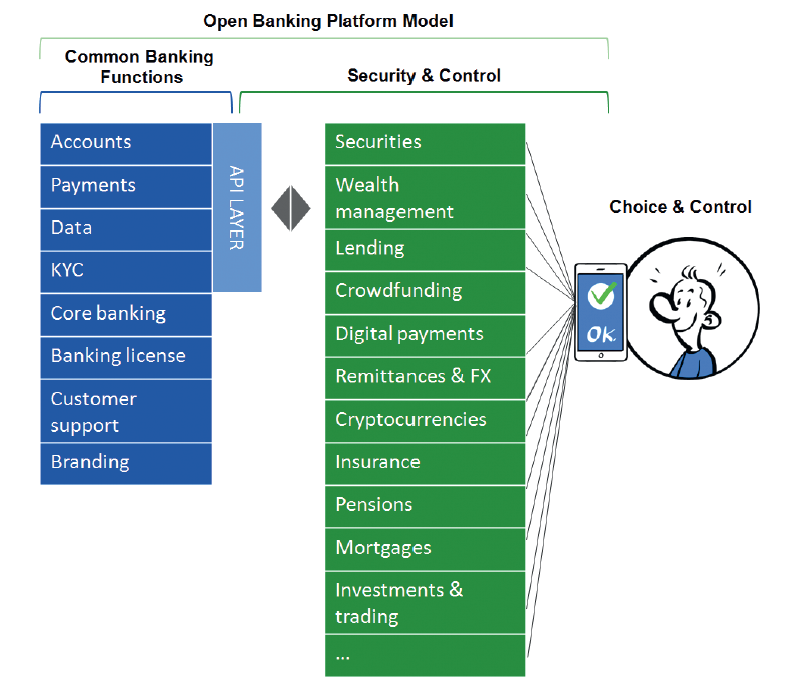

Their analysis of these three dimensions shows deep understanding of the problems and opportunities in each area. The diagram, below, beautifully sums up the essence of the Open Banking Platform Model:

Source & Copyright©2017 - EBA

Strategic implications and who is in charge

The report then examines “the strategic implications of customer control through Open Banking for banking practitioners, and shows how Open Banking creates new opportunities in product creation and distribution with a focus on how this relates to customer.” An important part of this analysis, highlights two fundamental questions when the ‘API acts as pivot’:

1. Who is distributing my products, which I make accessible via my API, to existing and new customers?

2. Who is creating the products that I will be distributing to my own customer base?

These are two examples of the huge issues that Open Banking raises not just for banks and payment system suppliers, but for corporate treasury departments as well. It also shows how difficult and time consuming such resolution will be.

CTMfile take: Corporate treasury departments need to understand that Open Banking will affect them as well as the consumer. This report is essential reading to understand the potential of Open Banking, the role of the APIs and the role of platforms in the changing focus on customer centricity and what it COULD MEAN. This report, which is both elegant in its analysis and plain ugly in its use of English, e.g. Platformisation, doesn’t really address how the banks and third parties will bring it about in an orderly fashion, rather than the API and platform mayhem that beckons. Nevertheless, essential reading for all corporate treasurers.

Like this item? Get our Weekly Update newsletter. Subscribe today