Identifying & Investing Cash Surpluses

by Lisa Rossi, Deutsche Bank & CTMfile

There is a new norm emerging in the investment market for cash surpluses. Prior to the economic crisis in 2008, short term operating and reserve cash did not require significant amounts of attention. Now with current accounts earning little or nothing and the threat of potential charges looming, it is time for companies to review their investment criteria and investment strategies for short-term cash surpluses.

Companies need to understand:

i. their short term cash flow and cash availability (see checklist on ‘Achieving Full Global Visibility and Understanding of Your Cash’)

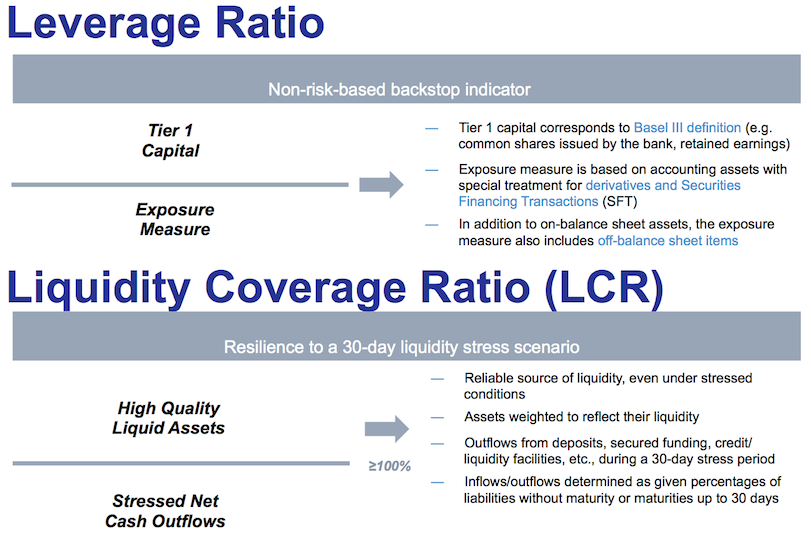

ii. the general impact of new bank regulations, particularly Basel III and the Liquidity Coverage Ratio, and how they will affect their cash and investment returns:

iii. the specific impact on:

- current account balances which now have varying degrees of value for banks, in some cases they can have a negative value in terms of calculating LCR value, viz:

- time deposits which lose LCR value as maturity date approaches, as chart shows:

iv.the new emphasis on investment products which comply with Basel III requirements e.g. call deposit or evergreen accounts

Finally, companies need to set up Passive and Active investment strategies to take advantage of new opportunities that will create value for their short-term cash surpluses.

This checklist takes the corporate treasury department through the key questions to be answered, the issues to be considered and the main actions required to manage the identification and investment of cash surpluses.

1. Become more attuned to the changing merits of the investment options available:

- current accounts balance: declining in importance as excess balances have little or no value. Keep only what you require each day for your normal disbursement schedules. Excess balances should be swept into investment accounts as specified by the company’s investment policy

- deposit accounts: becoming more important as new forms emerge, including evergreen/call deposit accounts which provide the opportunity to earn additional return over traditional time deposits for stable excess cash balances with open-ended maturity, N.B. companies have the opportunity to “call” the deposit within a set or established number of days to maturity

- money market funds: continuing to be a useful instrument even with the new proposed NAV regulations

- tri-party repos:becoming more important as they offer higher yields and are, in effect, a secured cash loan with the linked collateral

- commercial paper: long established product worth consideration in the new environment.

2. Review current investment policy given new market conditions, considering:

i. the compatibility of your policy with the investment products now on offer from the banks to encourage longer duration, e.g. if company policy only allows investment of cash for 30 days the company will not be able to place funds in new products focused on 30, 60 and 90 days

ii. risk criteria and how collateral can be used to offset risk

iii. the company’s overall investment instrument policy including:

the scope of the policy: how it relates to other treasury policies, the investments covered, other entities in the group covered by the policy and the sources of corporate cash covered by the policy

investment objectives which need to be defined including: security – the acceptable level of risk to principal; liquidity – the minimum liquidity standards, and yield – the benchmark figures for an acceptable yield and the proportion to be held in fixed-rate instruments

iv. review investment guidelines:

instruments – list either: 1) the approved instruments and their tenor or, 2) the set of approved criteria, including tenor, that all instruments must meet, i.e. treasury does not have to go back to the Treasury Policy Committee each time a new instrument is to be used

framework defining: 1) the acceptable currencies and whether all investments should be evaluated in the company’s base currency, 2) the approach to managing interest rates risk, 3) the names of approved counter-parties or a set of approved criteria, e.g. credit ratings, for all counter-party risk with banks and non-banks, 4) how tax calculations should be included in any decision to invest

v. review decision making responsibilities: how the company is regulated and the affect of this on investment policy and criteria

vi. review reporting: how the corporate treasury department reports on its investment activities and to whom, e.g. to the board, investment committee

vii. which investments can be fully automated (passive investment) and which types of investment require (active) treasury involvement.

3. Install efficient systems infrastructure and processes for investment execution:

i. segregate duties in the investment process to minimise potential for fraud

ii. choose which system and services to use for tracking and monitoring investments, options could include:

the treasury management system

stand-alone system and services

bank(s) systems and services

iii. determine how to assess the risk of each investment

iv. use an investment portal to minimise administration and risks in investing:

choose whether an omnibus or direct/fully disclosed portal will be used

ensure a full audit trail for each investment.

4. Maximise your fully automated investment (Passive Investment) by:

i. defining which cash balances can be invested automatically in a solution that fits your pre-defined investment criteria, e.g. Agent Repo solution from Deutsche Bank

-

Source & Copyright©2014 - Deutsche Bank

ii. ensuring all current accounts have an automated mechanism to sweep into interest earning instrument(s), e.g. off-shore money market funds

iii. ensuring that there are sound controls and counter balances, e.g. how and when investments are reviewed

iv. finally continuously searching for ways to increase the level of fully automated investment, e.g. some leading corporate treasury departments now invest up to 75% of their operating cash automatically.

5. Optimise your Active Investment execution by:

i. defining what due diligence is required with each new investment, e.g. controls and approvals, alerts required

ii. ensuring that full information is available on the availability of your cash balances and their tenor

-

- Source & Copyright©2014 – Deutsche Bank Liquidity Manager

iii. using automated services to identify opportunities to obtain better returns, e.g. Bloomberg, Thomson Reuters

iv. using investment portal(s) to execute investments, e.g. MyTreasury investment portal screen showing money market fund options:

- Source & Copyright©2014 - ICAP

v. looking for new ways/systems to automate active investment in the pre-trade, trade and post-trade processes:

- · Source & Copyright©2014 - Deutsche Bank

e.g. Hewlett Packard put in place a combination of systems and data sources to enable them to model and manage their portfolios, carry out scenario evaluations, and process and distribute their reports:

·

o Source & Copyright©2013 - Hewlett Packard Inc

Co-developed with Lisa Rossi, Managing Director Global Head of Structured Liquidity Products, Deutsche Bank

Like this item? Get our Weekly Update newsletter. Subscribe today