UK: Cash retains its crown while contactless card usage is booming and limit increased

by Kylene Casanova

Cash remains the most commonly used payment mechanism in the UK, according to the Payments UK. It is highly valued by consumers from all walks of life for its familiarity, wide acceptance and speed of transaction. During 2014, over 18 billion payments were made in cash, accounting for 48% of all payments made in the UK, worth around £250 billion. For payments made by consumers 53% were made by cash.

Role of cash

In the UK the role of cash varies dramatically between sectors:

Source & Copyright©2015 - Payments UK

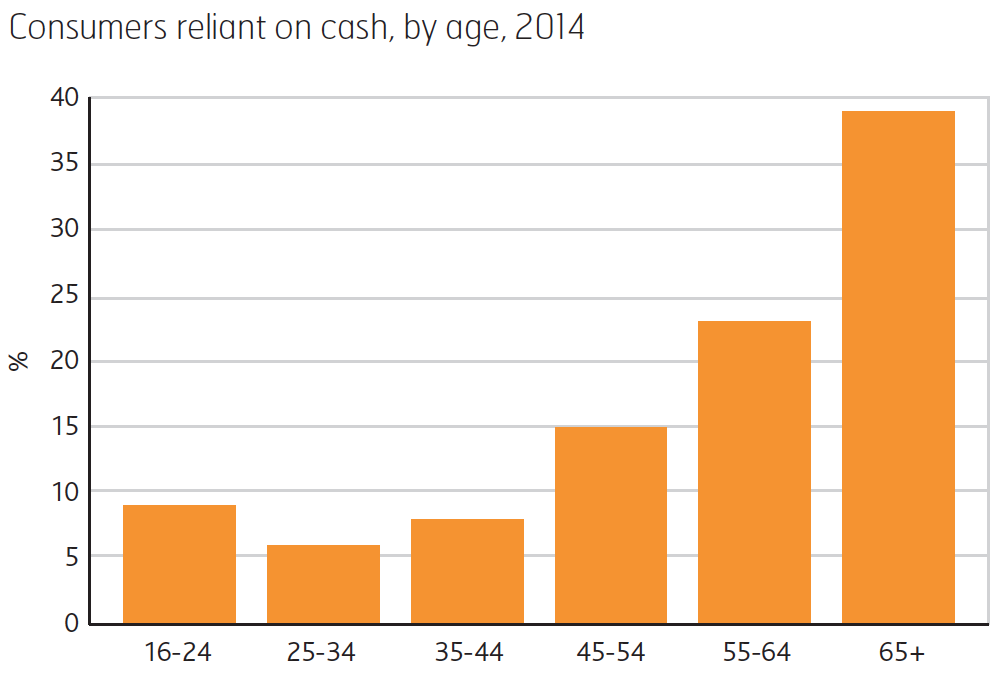

Also consumers reliance on cash varies by age:

Source & Copyright©2015 - Payment UK

Cash still dominates and is cheapest according to BRC

The British Retail Consortium annual payments survey for 2014 showed that average transaction values are declining:

Source & Copyright©2015 - British Retail Consortium

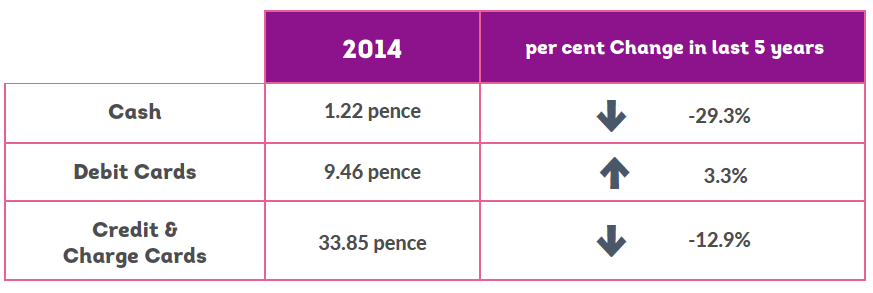

The British Retail Consortium are still claiming (not everyone agrees with this) that the average cost of a cash transaction is the cheapest (1.22 pence) and credit cards the most expensive (33.85 pence) method of collecting payments at point of sale:

Source & Copyright©2015 - British Retail Consortium

Booming usage of contactless cards

Contactless payment card usage is booming in the UK - in the first six months of 2015 more was spent on contactless cards than in the whole of 2014. This month the transaction limit was increased from £20 to £30. But this booming usage, contrary to what might be expected, does not seem to be significantly affecting the cash transaction share. Why is this? The simple answer is that while consumers are enthusiastically adopting contactless, they’re using the contactless function in their debit and credit cards to speed up the transaction whilst keeping it on their card accounts – not to avoid paying with cash.

CTMfile take: The lessons from the UK payment market development is that most retailers: will still need to accept cash; should accept contactless cards where they have high volumes of payments below the local transaction limit; and should encourage their trade associations to continue their campaigns against the high credit/charge card fees.

Like this item? Get our Weekly Update newsletter. Subscribe today