Who is responsible for detering payment fraud & cyber risk?

by Jack Large

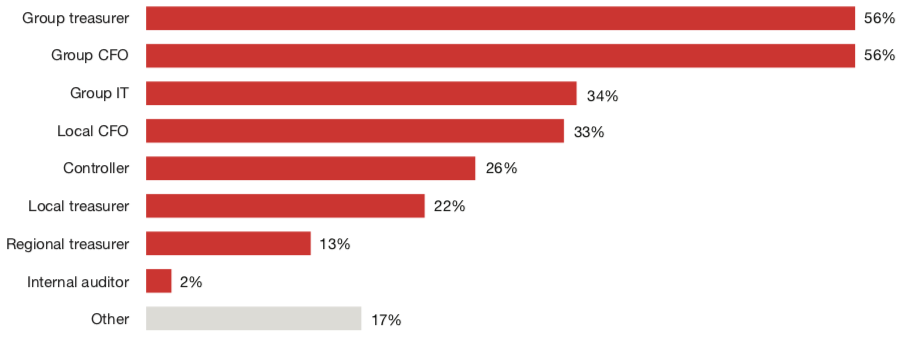

PwC’s 2019 Global Treasury Benchmarking Survey, see, found that only 15% of the 181 companies surveyed had no fraud in the last year while 9% had daily fraud attempts. When respondents were asked about who is responsible for payment fraud risk in your organisation:

Source & Copyright©2019 - PwC

How can treasurers deter payment fraud and cyber-attacks?

PwC advises that “Effective protections utilise a layered combination of defences that reinforce each other.” Best practices include:

- Raising awareness of employees. Many frauds are facilitated by simple human error or social hacking, so staff vigilance is important.

- Managing process and controls. Consider approved payment methods (e.g., no paper-based or voice-only payments). Establish independent callback requirements for master data changes or large transactions.

- Securing technology. Centralise and secure bank communication (payment hubs) as a way to focus investment and expertise, and provide structure to payment processes. Switch off electronic banking systems when not required (e.g., after business hours).

- Collaborating with IT. Work with IT partners on minimum security controls around data encryption, authentication, ensuring robust interfacing, regular penetration testing, and adequate network segregation.

- Creating a disaster recovery plan. Work with IT and financial operations to have a plan that includes training employees and testing of scenarios.

- Advising the enterprise. Manage the disaster recovery plan and serve in an advisory role across departments.

CTMfile take: Commonsense and this excellent list will serve you well, but remember relentlessly sticking to it is essential.

Like this item? Get our Weekly Update newsletter. Subscribe today