Bankers really understand payments

by Jack Large

Bankers are, mostly unfairly, given a hard time about not understanding payment systems and how they work, and what is going on. The report - “Cross-border retail payments” from BIS Committee on Payments and Market Infrastructures disproves this big time, e.g. the figure below.

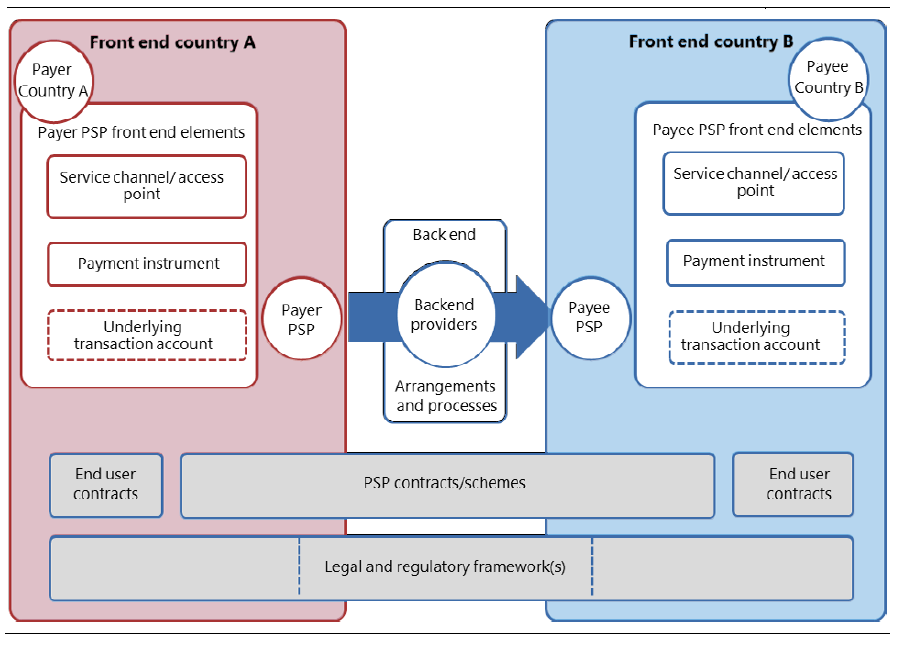

Stylised overview of the cross-border retail payments marke

Source & Copyright©2018 - CPMI BIS

The report explains that, “This overview of the cross-border retail payments market. Although it omits certain details, it depicts the demand side, ie the end users (the payer and payee), and the supply side, comprising the “front“ and “back“ end. The front end is made up of the interfaces provided to end users to initiate or receive cross-border payments as well as the payment service providers (PSPs) that interact with end users. The back end comprises the providers, arrangements and processes to effect those transfers, including associated foreign exchange transactions. Underlying everything are the contracts, schemes and legal and regulatory frameworks.”

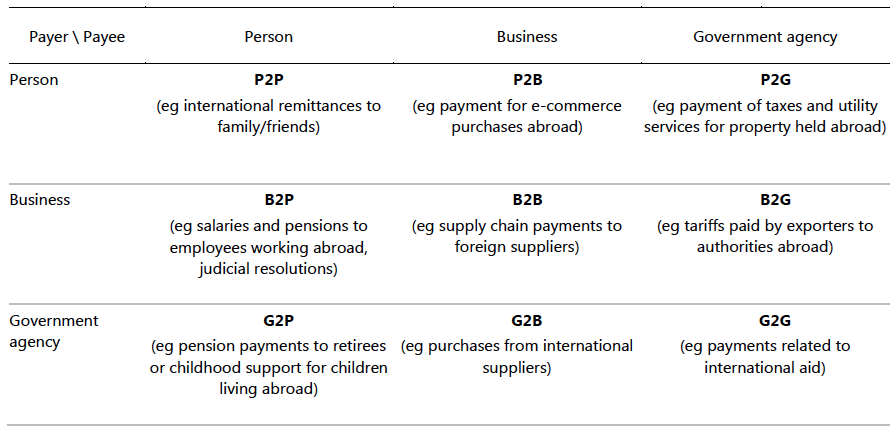

The demand side

End users differ across payment types in terms of their needs, requirements and capabilities. The report distinguish between different combinations of types of end users, and the main types of cross-border retail payments:

Source & Copyright©2018 - CPMI BIS

Supply side

The report then covers the supply side of retail payments and role of the different parties and their relationships The figure below on the back-end of cross-border payment arrangement shows clearly where the pressure points (for banks) in cross-border payment:

Source & Copyright©2018 - CPMI BIS

The report highlights how Distributed Ledger Technology could impact cross-border retail payments in two areas:

- Correspondent banking

- FX clearing and settlement.

And how the contractual, legal and regulatory framework could be impacted.

Findings

The report works through the findings in each area of retail cross-border payment services. The most interesting are the findings on the emerging alternatives to the established correspondent banking models where they highlight DLT, which is seen as a potential means to improve correspondent banking networks. But they say that, “Although several implementations are under way, it is an evolving technology that has yet to prove it is sufficiently robust to achieve wide-scale operation.” However, there are two other notable back-end models already operational:

- initiatives to link domestic payment infrastructures, e.g. the Directo a México, involving linkages between the United States and Mexico, has processed more than 4.9 million ACH payments, worth more than USD 2.6 billion, since its launch in 2003

- closed-loop systems proprietary: the cross-border retail payment study group feel this is one that seeing the fastest growth.

Overall conclusion

The report concludes that, “having more diversity of back-end clearing and settlement arrangements could result in cross-border retail payments that are quicker, cheaper and more transparent. Such diversity could include an improved traditional correspondent banking system, greater interoperability between domestic payment infrastructures and greater interoperability between closed-loop proprietary systems.”

CTMfile take: This report is worth downloading and studying. Bankers do know their payments.

Like this item? Get our Weekly Update newsletter. Subscribe today