How cost of capital is reshaping risk, regulation, and capital allocation

by Pushpendra Mehta, Executive Writer, CTMfile

Pushpendra Mehta, Executive Writer, CTMfile

In today’s environment of persistent volatility, cost of capital is no longer just a technical input into valuation models—it is becoming a multi-dimensional signal of how corporations perceive, price, and manage risk.

The Association for Financial Professionals 2026 AFP® Cost of Capital Survey Report reveals a subtle but important shift: companies are not only recalibrating how they calculate cost of capital, but also embedding it more deeply into risk frameworks, regulatory considerations, and decision discipline. For corporate treasury, this evolution signals a move from calculation to interpretation and strategic application.

Three interconnected developments stand out.

Cost of capital is increasingly being used as a dynamic risk-adjustment mechanism

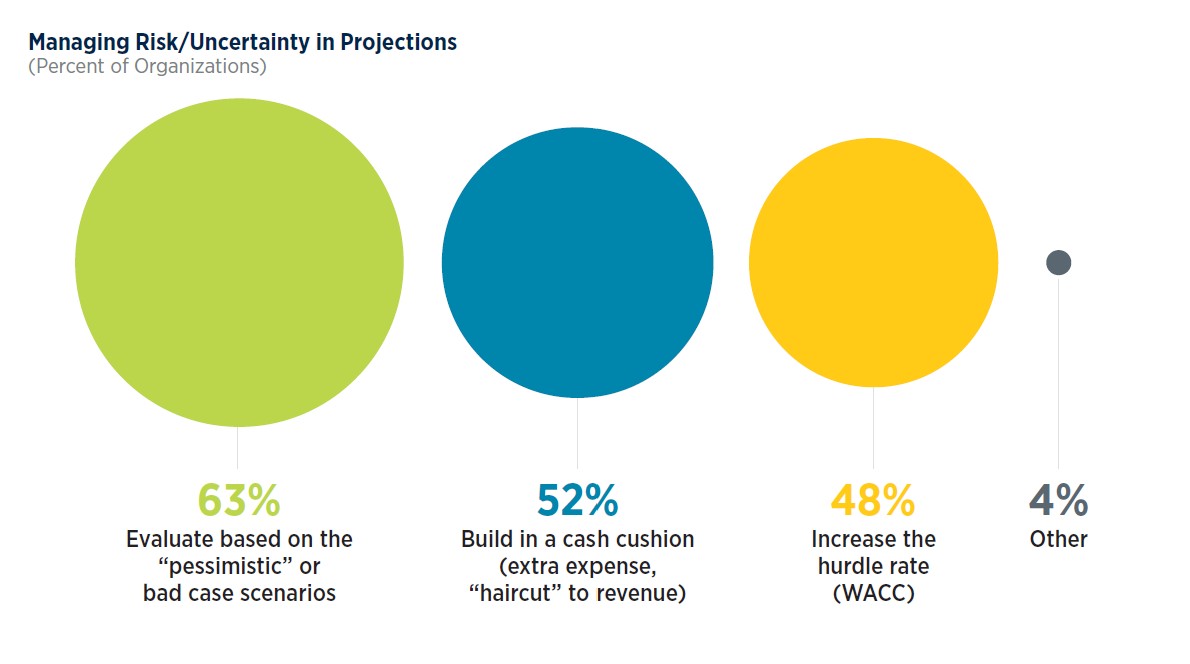

While traditional frameworks treat cost of capital as a relatively stable benchmark, the AFP survey shows that organizations are actively modifying it in response to uncertainty and project-specific risk.

Source: 2026 AFP ® Cost of Capital Survey Report

According to the AFP Cost of Capital Survey Report, 48% of organizations increase their hurdle rate (WACC) as a direct response to uncertainty, while 63% rely on pessimistic or worst-case scenario analysis when evaluating projects. This highlights a clear trend: cost of capital is being used not just to evaluate investments, but to absorb and reflect uncertainty.

Importantly, adjustments are not limited to macroeconomic conditions. The survey notes that 54% of organizations setting hurdle rates above cost of capital do so to account for unique project execution risks, such as country, currency, or geopolitical risks.

Taken together, these findings reinforce the need for corporate treasury teams to move beyond static weighted average cost of capital (WACC) calculations and toward scenario-linked capital frameworks—where risk premiums, discount rates, and hurdle rates are dynamically aligned with evolving risk exposures.

Regulatory and macroeconomic forces are directly shaping cost of capital assumptions

Another key development is the growing influence of regulatory and macroeconomic variables in determining cost of capital.

The AFP survey finds that 67% of organizations identify corporate tax rates as the most significant regulatory factor impacting WACC, followed by industry-specific regulations (50%) and central bank monetary policy shifts (43%).

This underscores a critical point: cost of capital is no longer insulated from regulatory change—it is increasingly co-determined by policy environments.

For example, higher capital requirements or regulatory buffers can increase the effective cost of funding, while tax regimes directly influence after-tax cost of debt and capital structure decisions. As the AFP survey report notes, regulatory constraints can lead to higher credit spreads and borrowing costs, ultimately feeding into WACC calculations.

At the same time, geopolitical dynamics—already influencing 55% of cost of capital assessments—are amplifying this effect by introducing cross-border risk premiums and supply chain uncertainties.

For corporate treasury, the implication is clear: cost of capital must be continuously recalibrated not only for market conditions, but also for regulatory shifts, tax changes, and policy-driven cost pressures. This elevates treasury’s role in integrating macro, regulatory, and financial perspectives into a unified capital framework.

Capital structure choices are becoming more pragmatic—and less theoretical

A third, often overlooked shift is how organizations are determining the inputs that underpin cost of capital—particularly capital structure assumptions.

The AFP survey reveals that 69% of firms now use their current capital structure when calculating cost of capital, a notable increase from 57% in 2020. In contrast, reliance on target capital structures has declined from 33% in 2020 to 27% in 2025.

This signals a move away from theoretical or optimal capital structures toward practical, real-world financing conditions.

Similarly, when determining debt and equity weightings, nearly half of organizations (48%) rely on book value–based ratios (current book debt/equity ratio), while others incorporate market-based (current market debt/equity ratio) or hybrid approaches (current book debt/current market equity ratio).

These findings suggest that organizations are prioritizing simplicity, stability, and alignment with actual funding conditions over purely market-based or forward-looking assumptions.

For corporate treasury teams, this reflects a broader shift toward operational realism. In volatile markets, constantly recalibrating toward an “optimal” capital structure may introduce unnecessary complexity. Instead, anchoring cost of capital to current structures provides consistency and decision clarity, even if it sacrifices some theoretical precision.

Connecting the dots: From input metric to strategic signal

Taken together, these three developments point to a fundamental transformation in how cost of capital is understood and applied within enterprises. It is no longer confined to being a valuation input or a technical calculation owned by the finance function. Instead, it is emerging as a strategic signal—one that reflects how organizations price risk, respond to regulatory and macroeconomic forces, and anchor decision-making in real-world capital structures.

As the AFP survey report notes, cost of capital “helps companies determine whether a project will provide returns to themselves and their investors.” Increasingly, however, it is also shaping the level of conviction behind those decisions—serving as a forward-looking indicator of how organizations interpret uncertainty, rather than simply measure it.

Conclusion

For corporate treasury, this evolution carries significant implications—expanding its role from calculating cost of capital to actively shaping how it is applied in strategic decision-making. This shift requires treasury teams to move beyond technical precision and toward decision stewardship—ensuring that capital allocation reflects not only financial thresholds, but also risk context, regulatory realities, and strategic priorities.

In practice, this means continuously recalibrating cost of capital frameworks to reflect changing market conditions, challenging underlying assumptions where necessary, and maintaining alignment between capital structure, risk appetite, and investment decisions.

In this context, cost of capital is becoming a living metric—dynamic, contextual, and central to how organizations navigate uncertainty. For treasury leaders, the opportunity lies in using this evolution to drive greater discipline, sharper decision-making, and more resilient capital allocation across the enterprise.

Like this item? Get our Weekly Update newsletter. Subscribe today

About the author