Nafta’s impact on supply chains and FX: a tale of north and south

by Kylene Casanova

Renegotiating the North American Free Trade Agreement (Nafta) was one of President Trump's key election pledges. How will it impact corporate supply chains, FX and cash flows?

The US is sandwiched between two unequal partners. To the north it has a stable, prospering economy and an important source of oil imports, while to the south, Mexico's cheap labour and lower costs are perceived as taking employment and manufacturing away from the US. And yet all three markets are bound by the same free trade agreement and all three markets are interdependent in terms of trade, manufacturing and employment. FX strategist at Credit Agricole, Vassili Serebriakov, says: “Every car from Canada has parts from Mexico, Canada and the US, so those global, integrated supply chains will be threatened even if the principle target [of a revised Nafta] is Mexico.”

It's unlikely that the US will want to dismantle Nafta completely but the Trump administration will certainly push to renegotiate the agreement to align more closely with US economic interests, in order to boost domestic investment and employment. Two of the key points the US will push for under Nafta are:

- lower US corporate tax rates; and

- a tariff on industrial goods of 7.7 per cent for US manufacturers exporting to Mexico.

Peso sensitive to tweets

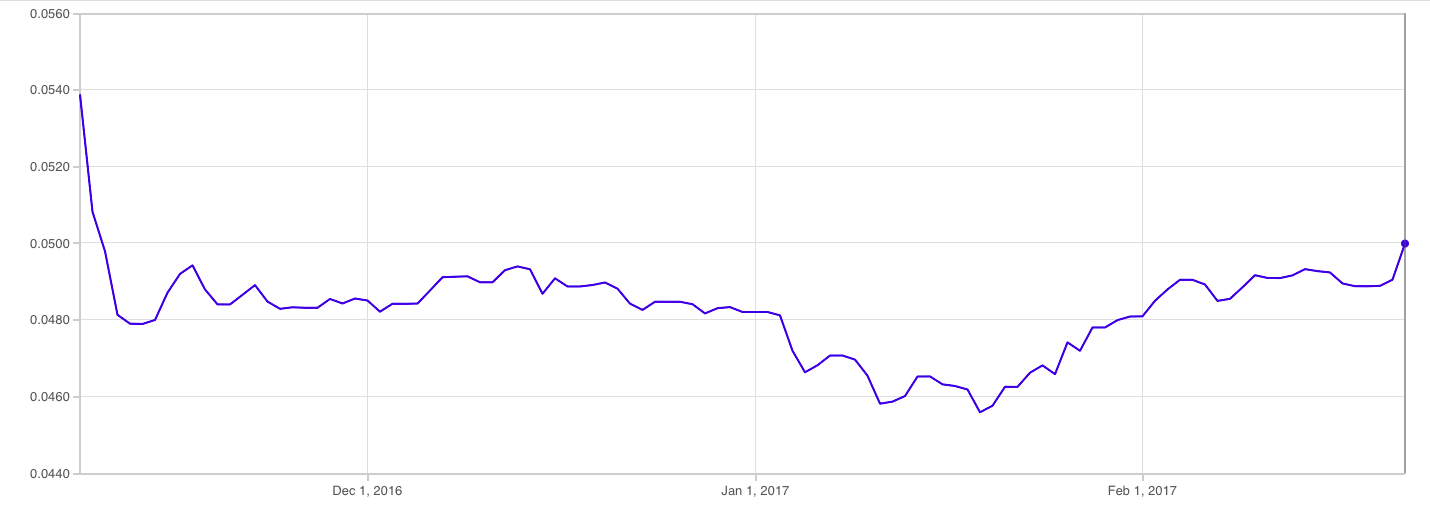

The outcome of future Nafta talks remains to be seen but one of the more immediate issues for corporate treasurers is the FX volatility that this uncertainty around Nafta is creating, particularly for the peso. On election night, on 8 November 2016, the falling value of the peso was the first major financial indicator of a Trump win – even before all votes had been counted.

Since Trump's win the peso has seen considerable volatility and has been very sensitive to the ups and downs of the new administration. Oanda's Natasha Lala, writing in Treasury&Risk, says: “Dollar-peso exchange rates have been pivoting on every word (and tweet) from the new American leader. Early indications suggested that a Trump presidency would be catastrophic for the peso, with the dollar soaring to record highs against Mexico’s currency. Since then, though, the peso has rallied on the belief that Trump’s brand of protectionism might actually favor a weaker, more affordable dollar.”

This graph shows how the peso-dollar value has fluctuated since 8 November last year, losing about 7.4 per cent of its value since then.

Treasury needs to be part of the conversation

But the dollar-peso exchange rate isn't the only consideration for corporate treasurers. A secondary result of any border tax on US exports to Mexico, combined with a stronger peso, could lead to higher production costs (wages, location overheads, raw materials) for manufacturers in Mexico. Company executives would certainly need help from their corporate treasurers to advise on how FX rates, tariffs and taxes will affect cash flows for the company. Oanda's Lala writes: “treasurers of multinational companies, whether large or small, need to be part of the conversation on operations decisions, particularly in a political situation as unpredictable and rapidly changing as our current environment.”

Canadian dollar could price in more risk

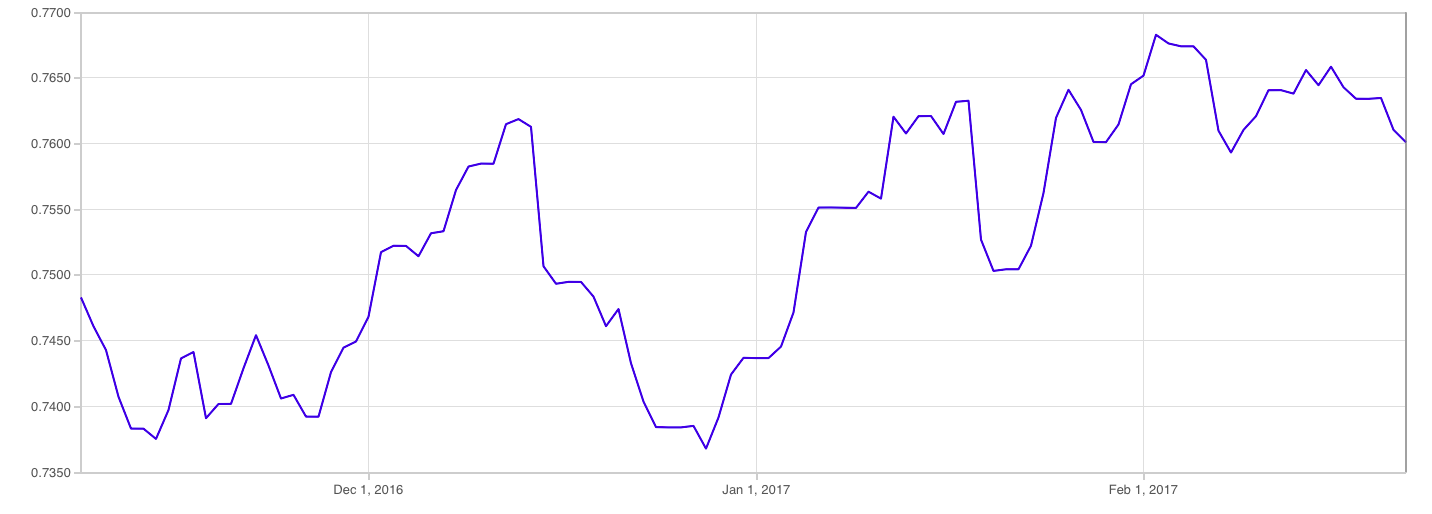

As for the Canadian dollar, the 'loonie' has shown considerable strength since the US presidential election, dipping below 0.74 US dollars before reaching its current value of 0.76 US dollars.

Observers of Trudeau's visit to Washington earlier this month might have noted that the Canadian President had a thing or two to teach Trump about the presidential handshake, but it seems that Canada's confidence is supported by its strong economic relationship with the US. As Credit Agricole's Serebriakov, told Bloomberg, the Canadian dollar has very low Nafta risk priced in. In contrast with Mexico, the US's trade with Canada is more balanced and Canada is a strategic oil supplier to the US market. He added: “That's why I wouldn't be completely relaxed from the Canada perspective and that's why the Canadian dollar should price in a little more risk than it does right now.”

Like this item? Get our Weekly Update newsletter. Subscribe today