Paym system in the UK could link all smartphones to mobile payments

by Kylene Casanova

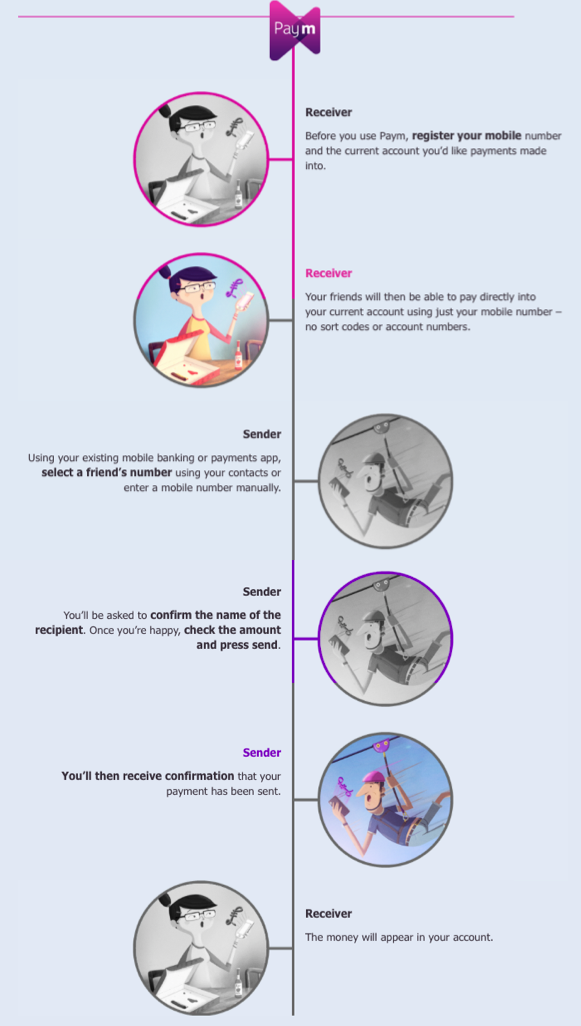

The idea is very simple, set up a database that links all smartphone numbers to the owner’s bank branch code (in UK called a sort code) and account number. Then within each bank’s mobile payment App all that is required to make a payment is to type in the recipient’s mobile number. The new system is called ‘Paym’, see figure below.

How Paym works

Source & Copyright©2014 - UK Payment Council

The system is operated by the UK Payment Council and payments are cleared via the Faster Payments or the Link ATM payment systems in almost real-time. At present, most of the major banks and building societies are live on the system, and by year end RBS, First Direct and a few other subsidiaries will join making 9 out 10 mobiles in the UK will be covered by the system.

The Paym system includes many safeguards to ensure that there is no fraud at key moments, e.g. when customers change their mobile number or change their bank. Particular attention has been given to ensuring that the mobile operators practice of recycling mobile numbers after 6 months if not used, does not cause any misdirected payments.

By 9 May, 500,000 mobile owners had registered, and 10Ks are registering every week. The Payment Council expects millions will have joined the Paym scheme by early next year when all UK banks will be Paym members.

Types of payment now and in future

At the moment Paym is being solely used for peer-to-peer payments, as the family example above shows.

However, it is easy to see how the service could be expanded to deliver business-to-consumer payments and consumer-to-business payments like those provided in Barclays Pingit scheme:

- collecting payments for purchases at shops and online, see

- making payments to consumers such as the Pingit ‘send a payment’ service, see.

These new services based on Paym won’t need any further inter-bank agreement, so we might see such services sooner rather than later.

The one thing that is for sure, once UK consumers have got used to making a payment by just typing in a mobile number, they won’t put up with anything that is much more complicated.

CTMfile take: Paym could be the catalyst to accelerate mobile payments in the UK. Corporate treasurers should ask their UK bank(s) what B2C and C2B services they are developing. Such services could cut your payment and collection costs considerably, and open up new market niches.

Like this item? Get our Weekly Update newsletter. Subscribe today