Top 10 mistakes that companies make in FX risk management

by Kylene Casanova

Atlas Risk Advisory provides foreign exchange (FX) risk management solutions for multinational corporations. Their executive team has a combined 60 years of experience in FX risk management and based on they issued a white paper in October 2012 listing the ’Top 10 mistakes in FX risk management’, which describes the very basic errors conmpanies make:

- Maintaining the status quo: FX groups often have a lot of inertia around their current practices, and fear of change can be a major obstacle. Because the stakes can be so high, the perceived “safety” of maintaining any current approach “because we’ve always done it this way” can be prevalent. The problem with this is that many things have likely changed since a certain practice was established, and various assumptions that may have been true many years ago are no longer true today.

- Taking a view on the direction of currencies: A successful hedging program shouldn't be influenced at all by directional views, or by the most recent trends that have occurred. Too often a hedging program is terminated because it's “losing money” just before the underlying exposure begins to lose value and the hedges (now non-existent) would have had offsetting gains. The success of a hedging program needs to take both the underlying exposure and the hedge into consideration when determining its effectiveness. Trying to guess what would happen to only one side of the equation is not effective risk management.

- Not engaging enough with business partners: If you hedge your company’s local currency revenue exposure, do you understand the competitive environment in the various geographies where you do business, and the specific pricing dynamics? Do you have any pricing power if there is a huge move in FX rates? A good way to test if a hedging strategy makes sense is to “stress test” it with different “What if?” scenarios, which should include some modeling on how you and your competition, suppliers, and/or partners would react. If you can’t live with the results of a significant currency shock in either direction, chances are your hedging strategy needs some adjusting.

- Having an aversion to locking in losses: This problem often occurs with balance sheet hedging. Let’s say you receive new information on an exposure a week after you set your monthly accounting rate. The nature of this information is such that you should enter into an outright forward to adjust your hedge. But if the currency has moved out of your favor compared to the accounting rate, the adjustment hedge will lock in a loss. Atlas conclude: “Volatility is a function of time, so a week’s worth of unfavorable volatility can turn into a month’s worth of far more unfavorable volatility. “Hope” is not a strategy. If an exposure is material, hedge it.”

- Having a poor balance sheet forecsating process: Atlas advise having a centralised process that derives the relevant balance sheet by taking the latest known actual exposure and build upon it with income statement inputs, which tend to have more ownership and accountability and should therefore have improved accuracy.

- Creating unnecessary volatility from liquidity management: Atlas recommend using even swaps to manage liquidity needs, as this avoids unnecessary spot rate versus accounting rate impact, and eliminates the need to guess on collections or payables timing.

- Relying too much on spreadsheets: A monster spreadsheet can only be navigated by the person who built it, use an FX management platform to manage all the complexities of FX exposure management.

- Paying too much when trading FX: Atlas recommend trading off of “fixing rates” is the best way to get the most transparency from the banks.

- Relying solely on an ISDA for managing your counterparty risk: ISDA (International Swaps and Derivatives Association) agreements have been commonplace for many years, but as Lehman demonstrated in 2008, these almost always benefit the banks more than the corporate side. Atlas advises corporates to think of using a third-party collateral manager and exchanging collateral beyond a tolerable threshold with their counterparties, or possibly moving the “core” exposure to a futures exchange. The objective is to ‘take the counter-party risk of the table’.

- Not understanding your FX results in a timely manner: Companies need the ability to manage the mismatch between the underlying exposures and the hedges meant to neutralize them for a number of reasons. Altas believe it is critical to understand your results and have a quick feedback loop for your next period’s hedging.

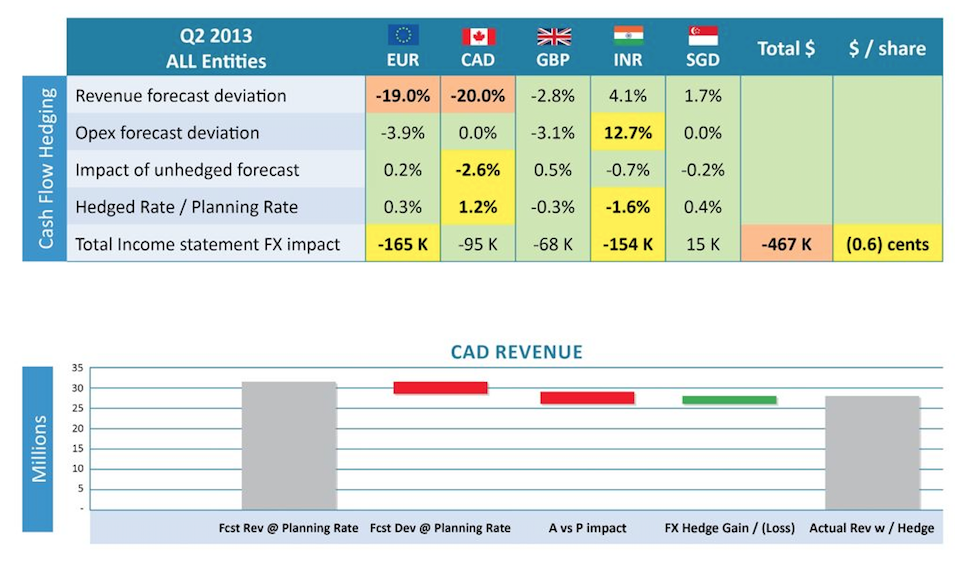

AtlasFX® Cash Flow Dashboard

AtlasFX’S lead product, is a cloud-based software solution that provides best practice Income Statement and Balance Sheet Exposure Management by integrating ERP and TMS information with exposure aggregation, risk quantification, and results analytics. The latest version of their Cash Flow Dashboard helps solve the 10th problem above of not understanding your FX results in a timely manner:

Source & Copyright©2014 - Atlas Risk Advisory

* * *

CTMfile take: This useful list of 10 common mistakes in FX risk management shows that effective FX exposure management is all about sound practices and having the appropriate tools.

Like this item? Get our Weekly Update newsletter. Subscribe today

I like the second point Taking a view on the direction of currencies.You have rightly mentioned that we should consider both the underlying exposure and the hedge while determining the success of a hedging program.