Two key trends affecting corporate bond liquidity

by Kylene Casanova

A report by Greenwich Associates, Corporate Bond Liquidity Solutions Emerging, looks at changes in investor behaviour in the fixed-income markets, which are being transformed by e-trading and improved liquidity intelligence.

It paints a picture of a very competitive corporate bond trading landscape in a state of flux, with a flurry of new corporate-bond related technology initiatives coming on the market in recent years, only for many of them to close or restructure.

Growth of e-trading

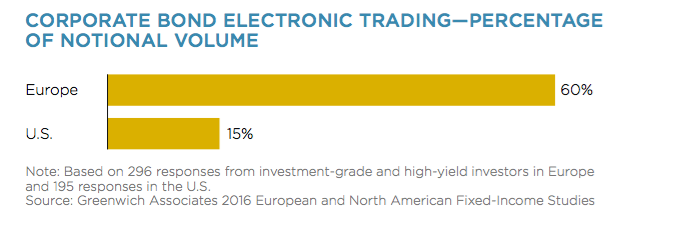

Electronic trading continues to grow in the US and Europe and now accounts for 60 per cent of trading in Europe and 15 per cent in the US.

The report's authors write: “Trading via the traditional request-for-quote model has grown, as has trading via models newer to corporate bond investors, including auctions and all-to-all crossing networks.”

However, the report also reminds that, although e-trading is a growing part of the market, the majority of trades are still processed manually: “Remember that as e-trading in corporate bonds is growing, over 80% of the roughly $6 trillion traded annually in the U.S. market is still matched and executed over the phone or via instant messenger. With trading desks on both the buy and sell side now smaller, technology to help the high-touch business is needed as well.”

Reduced market liquidity impacting buy-side strategy

The report also notes that investors are still showing signs of anxiety regarding corporate bond liquidity. It notes: “Of the more than 400 credit investors interviewed by Greenwich Associates in the U.S. and Europe in 2016, over 80% still feel that reduced market liquidity is impacting their ability to implement their investment strategy.”

Market players

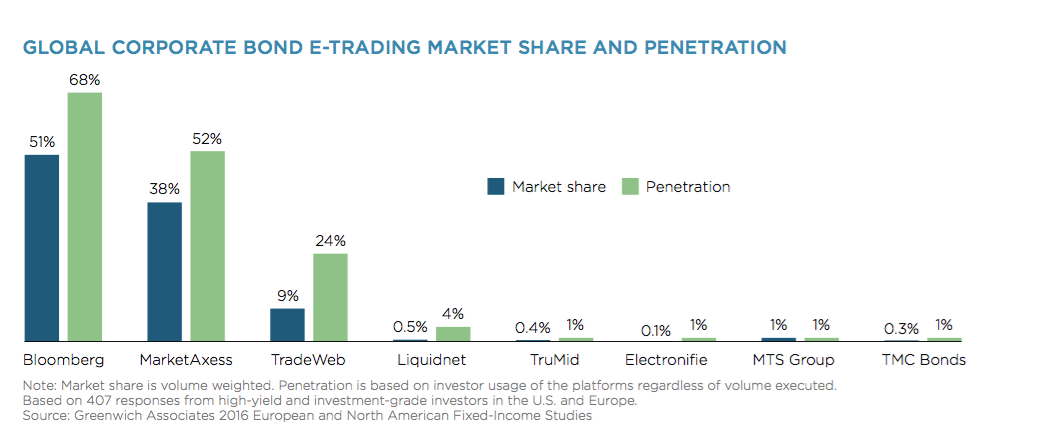

Greenwich Associates' report also looks at the main players in the European and US markets, which are dominated by MarketAxess and Bloomberg. The graph below shows market share and penetration for eight of the main e-trading platforms.

Pricing data expected to grow

The report also sets out how the pricing of corporate bonds can be expected to develop. Bloomberg, ICE and MarketAxess currently provide continuous prices for the majority of corporate bonds in the market. Greenwich Associates writes: “Given the reputation of each of those firms, we can comfortably say the quality of the data will only grow. However, in a market where dealers are less willing to make prices in general and investors are increasingly able to place resting orders with price limits into the market, a source of conflict-free theoretical pricing can help encourage trading where none would have happened before.”

The two prevailing trends in the corporate bond market highlighted in the report are the moves towards platforms that enable better connections for investors and traders – such as all-to-all trading platforms – and increasing data services that provide more information – liquidity intelligence – on corporate bonds. The report states: “But relationships can be improved with better information and more efficient means of connecting.”

CTMfile take: This report focuses on the buy-side but for corporate bond issuers, it provides an interesting overview of how the trends in the market are affecting liquidity and pricing. The main two trends highlighted are how e-trading initiatives are provided improved connections between market participants and how technology is providing better liquidity intelligence.

Like this item? Get our Weekly Update newsletter. Subscribe today