Working Capital Foundations: Measure of Solvency

by CTM News Team

This is the first article in a mini-series about working capital management and supply chain finance. Treasury is responsible for liquidity management, and the cash conversion cycle has a major impact on working capital.

There are two common definitions of working capital, and these originate from different perspectives and serve separate purposes. Understanding these different definitions and purposes matter. We’ll begin with the accounting and banker’s definition of working capital. It can be expressed as a formula:

Accounting/Banking: Working Capital

Current Assets – Current Liabilities = Working Capital (accounting)

This definition provides a basis to show that an organization has the ability to cover its current obligations as they come due. Do you have enough cash and receivables that will convert to cash (current assets) to cover your accounts payable obligations, payroll, and near-term debt payments (current liabilities) as they come due? This formula provides a top-level measure for how an organization can satisfy those obligations.

To an extent, the larger your working capital number, the better position the organization is in to cover their obligations as they come due. Negative working capital can indicate pending insolvency, a challenging period, or the need to secure more credit immediately.

Everyone can agree that cash is better than a receivable since you can’t make a payment with a receivable (we’ll talk about using receivables for liquidity later in this series). In this formula and definition, when a client pays you, your accounts receivable (AR) converts to cash, which is simply swapping one current asset (AR) for another current asset (cash).

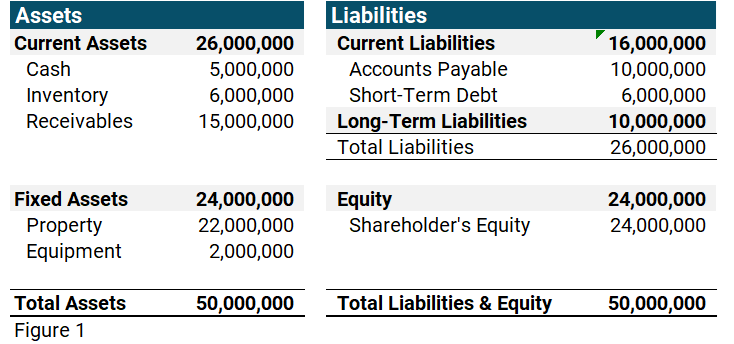

For example, we’ll begin with the balance sheet in figure 1.

Balance Sheet. As of xx/xx/xxxx

Running our formula of: Current Assets – Current Liabilities = Working Capital

$26,000,000 - $16,000,000 = $10,000,000

We find we have $10mm of working capital. This is the excess of current assets over current liabilities. Note that in this case, there is $5mm to cover $16mm of AP and S/T debt obligations, so timing will be important.

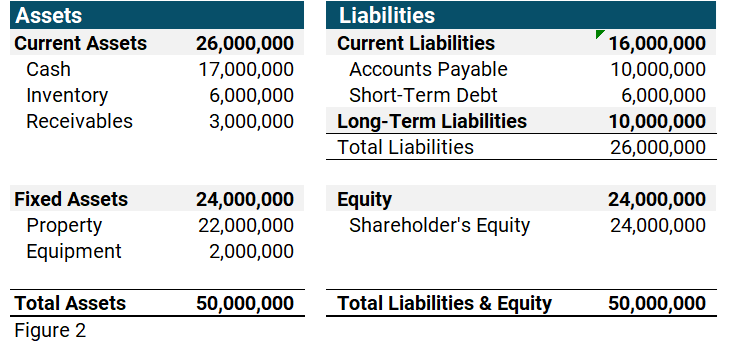

The company’s clients now pay $12mm on their account, which reduces the receivable while increasing cash. Let’s take a quick look at the balance sheet in figure 2, which reflects this activity.

Balance Sheet. As of xx/xx/xxxx

Running our formula of: Current Assets (CA) – Current Liabilities (CL) = Working Capital (WC)

$26,000,000 - $16,000,000 = $10,000,000

We see that we have the exact same amount of current assets, $26mm, and the same amount of working capital ($10mm) as before. Again, this $10mm represents the excess of current assets over current liabilities. Now, there is $17mm in cash to cover $16mm of AP and S/T debt obligations. This puts the company in a better position in the short-term from a liquidity standpoint.

The purpose of this formula is not about cash scheduling or the efficiency of the cash conversion cycle It is a simple measure that allows others to get a picture of the organization’s ability to meet current obligations as they come due. This has strong utility for lenders and accountants providing a macro view, and it is easy to calculate since we can use our financial statements (balance sheet) to capture this information at any point in time.

In the next installment, we’ll cover the treasury definition of working capital.

Like this item? Get our Weekly Update newsletter. Subscribe today