Yet another report telling the banks what to do on payments

by Jack Large

It is conference season - EuroFinance, AFP and the SIBOS, so all sorts of consultancies, laudable organisations, banks and SWIFT do their research and time their publication to be ready for the “season of mists and exciting (?) conferences”. The latest publication to reach CTMfile is the 13 page white paper by BCG and SWIFT “International payments: accelerating banks’ transformation” which has various findings, those which could be of interest to corporate treasury departments, include:

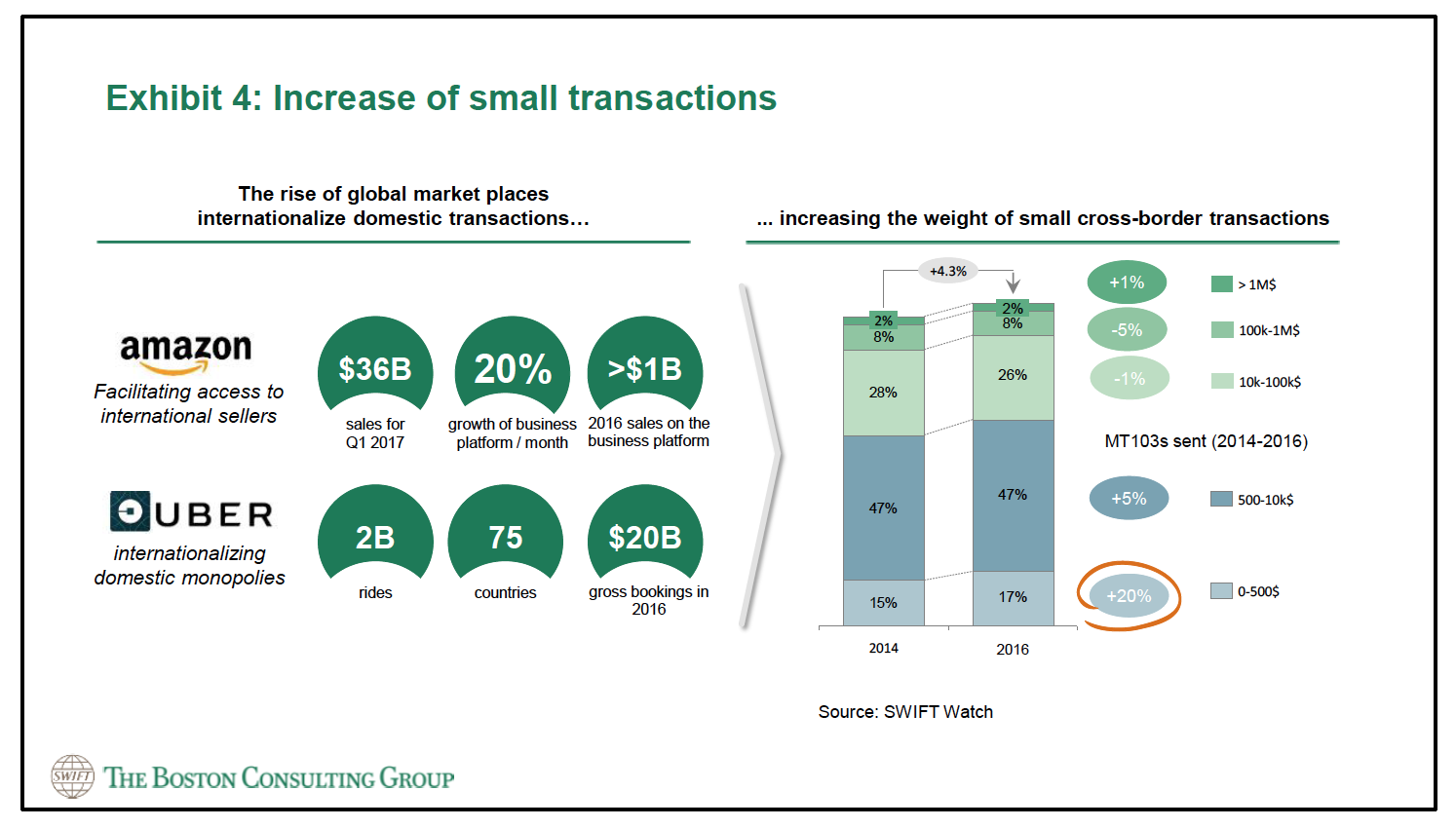

- Rising global market places blur the frontier between payment and purchase processes:

- Online marketplaces and e-commerce platforms, such as Uber, Amazon and Alibaba, are weaving payment – domestic and international alike - into a seamless purchase process, making the payment step invisible to the customer. And because several of them have global business models, they are turning historically domestic flows, such as taxi or take-away food purchases, into international transactions. Even on SWIFT, typically more used for higher value corporate payments, cross-border payments under $500 have grown by 20% since 2014.

- Trend of shrinking average payment size will continue, similarly to what the industry has seen in securities markets with the improvement in technology and the reduced friction in processing small transactions.

- Regulatory activism is consolidating correspondent banking:

- Seventy-five percent of global banks have withdrawn from some correspondent banking relationships and the number of active corridors declined by 6.3% between 2011 and 2016.

- This is especially reducing the coverage of high-risk and low-volume regions, such as the Caribbean, Africa and Polynesia, which already have fewer correspondent banking relationships.

- Data enriched flows and STP are embedding payments within business processes:

- Enriched data flow standards (ISO20022) and straight-through-processing (STP) allow banks and tech players to offer value-added services inspired by the likes of Uber and Amazon “one click shopping experiences”.

- For corporates, they enable the further integration of corporate payments into other business solutions. TMS/ERP providers can go beyond their current value proposition and integrate payments into sourcing, shipping, inventory management and customer acquisition.

- With payments increasingly melting in other processes, interconnection and interoperability become key features of payment infrastructures.

- Banks’ prospects in the new international payments environment are not good as:

- Costs are rising and charges are under threat from tech giants and digital challengers

- To survive in the face of increased regulation and competition, banks will need to invest in emerging technology and in providing improved services to their clients:

- Global transaction banking giants will experience the least difficulty. In fact, they are likely to gain market share because their scale means the unit costs of the required investments is lower for them than their smaller competitors

- small domestic banks will arrive at the destination to which they have been travelling over recent years. They will need to focus on “relationship banking”, providing services based on the trust gained from familiarity with their clients, and outsource their subscale international payments operations to larger players.

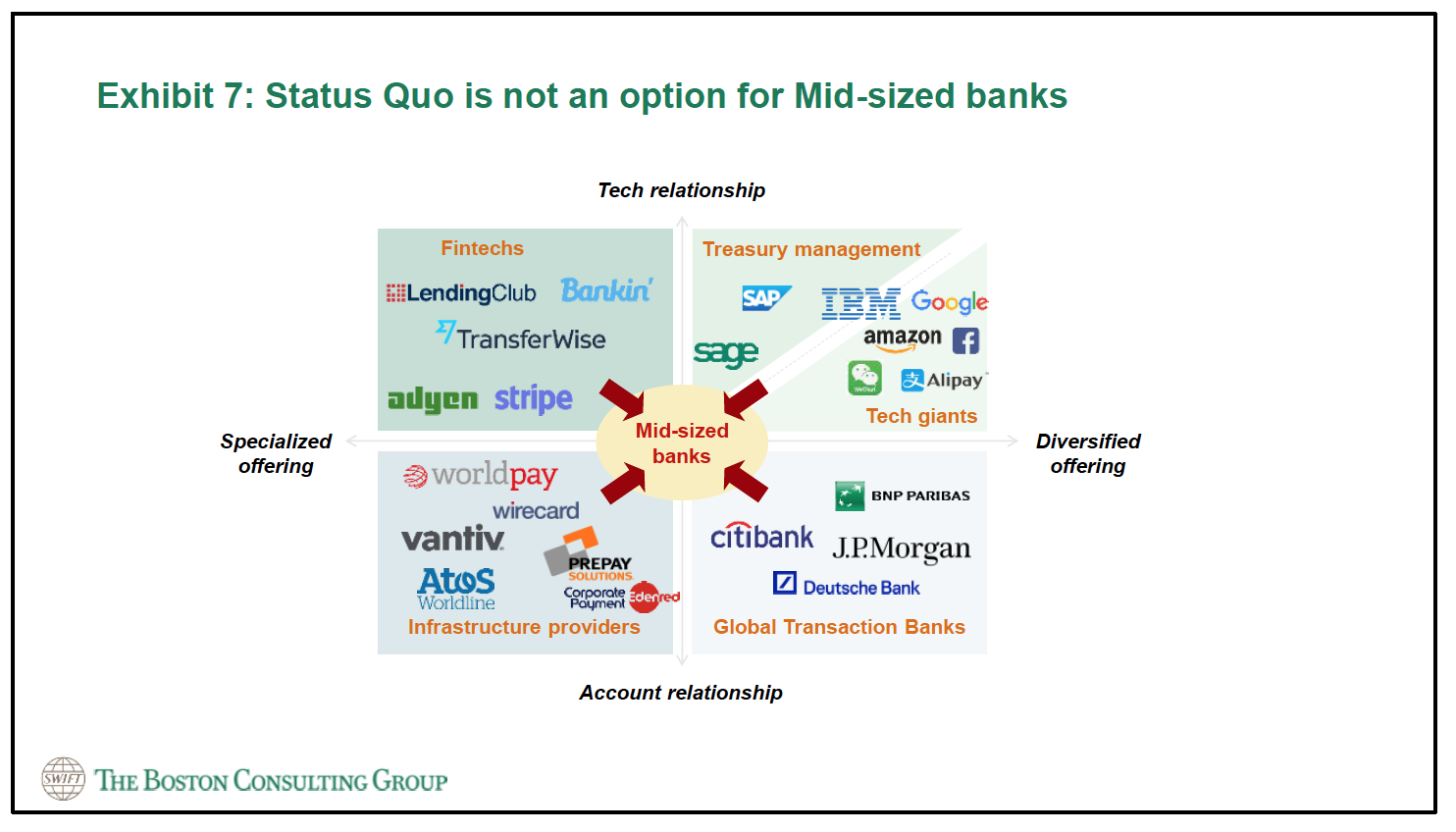

- situation of mid-sized banks is the most problematic, not only in international payments but more generally they are being squieezed from all sides:

- The emerging role of other players in international payments: FinTechs and other technology companies will continue to drive innovation in international payments.

Overall conclusions

On banks:

- “Banks can still win at the international payments game. However, they need to deeply transform their services and operations to gain agility, trust, reach and build a scalable model. Midsized banks, at the front row of international payments transformation, need to carefully consider their model and decide where they want to play depending on their current positioning.”

On corporates:

- “After years of dissatisfaction, corporate clients face an emerging world with scores of choices and better deals. But they also face growing complexity and increased risk. They will need to carefully decide how to trade-off speed, cost and risk when choosing their suppliers of international payments and related services. With the burden of compliance creeping from the financial sector and into the corporate world, they will increasingly need a trusted advisor to guide and support them, which creates additional opportunities for banks.”

CTMfile take: How sure are you that your banks will continue in the payments business, particularly your mid-sized banks?

Like this item? Get our Weekly Update newsletter. Subscribe today