Working Capital Foundations: Measure of Capital Use in the CCC

by CTM News Team

In this second article in our mini-series about working capital management and supply chain finance, we will explore treasury’s responsibility to manage liquidity. We’ll look at this by focusing on the elements of the cash conversion cycle (CCC).

As a refresher, there are two common definitions of working capital, and these originate from different perspectives and serve separate purposes. In the first article we looked at the banking/accounting definition. The treasury definition, which is also called net adjusted working capital (NAWC) is expressed in the following formula:

Treasury: Working Capital / NAWC

- Accounts Receivable + Inventory – Accounts Payable = Working Capital (treasury)

- AR + INV – AP = NAWC

The purpose of this formula is to highlight how much cash is tied up in the cash conversion cycle. The three components (AR, INV, AP) either use the organization’s cash (AR, INV) or use someone else’s cash (AP). This represents the liquidity that is tied up in running the core part of the business.

In using this definition or formula, the goal is neither to maximize nor minimize working capital. Maximizing WC (or NAWC) can easily be accomplished by extending receivable terms, loading up on inventory, and paying suppliers more quickly. However, this would be highly inefficient from a liquidity viewpoint and can lead to greater losses. Conversely, minimizing WC can be accomplished by cutting off all trade credit (bringing AR down), reducing inventory, and working to extend payment terms no matter the impact on pricing. This would reduce the ability of the business to sell, drive customers to competitors, and cause suppliers to increase pricing to compensate for being paid so late.

Optimization, or the right balance of these CCC areas, is the proper target. Extending trade credit to support good sales with worthy customers allows your company to have good top and bottom-line numbers. Maintaining an adequate inventory can support sales and prevent losses from customers choosing a competitor due to your lack of stock. Managing payables has some similar considerations, as your suppliers will react to notable changes or to practices that are more costly than with their other customers.

Reflecting on both definitions (accounting and treasury) is needed when answering this question: do you want to have more or less working capital? The answer depends upon which definition you are using and what you are trying to accomplish. For the accounting definition, finance wants to have enough liquidity to meet their obligations as they come due. For the treasury definition, you want the amount to be optimized to support good and profitable sales.

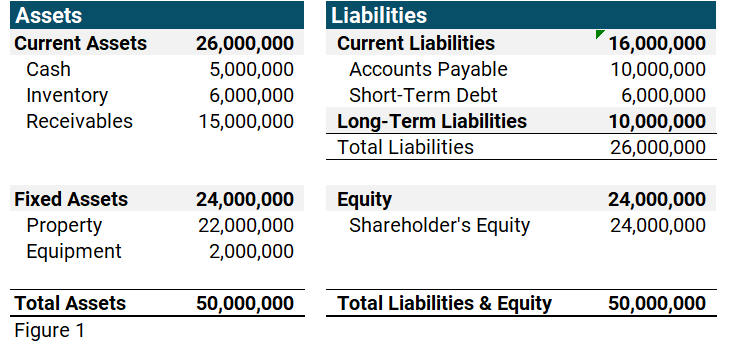

Consider this formula using the treasury definition of working capital with the balance sheet in figure 1.

Balance Sheet. As of xx/xx/xxxx

Running our formula of Accounts Receivable + Inventory – Accounts Payable = Working Capital (or NAWC)

AR + INV – AP = NAWC

$15,000,000 + $6,000,000 - $10,000,000= $11,000,000

The $11mm represents the liquidity, or cash, you have tied up in the cash conversion cycle. This is broken down as follows:

- Using $15mm for AR as you support your customers by funding their purchases for, perhaps, 30 days.

- Using $6mm for your inventory to support sales.

- Gaining $10mm with your AP as your suppliers help finance your CCC.

Most organizations will have a positive WC number. There are some businesses and companies that have a negative WC number. A negative number means they are gaining cash through the normal operation of their business. Here are a few examples:

- An airline collects fares for flights an average of 25 days before flights are taken. At $4mm per day of sales, this provides them with $100mm of cash earlier in the process (helping the accounting definition but not the treasury definition) and means that their AR may be close to zero (improving the treasury definition).

- A manufacturer works out a buy-as-consumed arrangement with its suppliers. This reduces inventory on their balance sheet. It also means that the suppliers have a larger inventory, as they are funding the manufacturer’s balance sheet.

As has been shown, the treasury definition of WC captures how much cash is tied up in the processes that allow a company to make goods and sell them to their clients across AR, INV, and AP.

This understanding is foundational for two key reasons. First, it allows us to understand the different terms and purposes in contrast to the accounting definition, supporting better communication. Second, it provides a basis for understanding how efficiency in the cash conversion cycle matters to organizations.

The next article will cover measurements of efficiency in the CCC. We will shift the primary focus from a currency total (dollars in the case above) to days. The efficiency measure is certainly important from a general business perspective. However, we will also see how it has a reflective impact on how much cash is needed for the operation, whether it is static, growing, or shrinking.

Like this item? Get our Weekly Update newsletter. Subscribe today