Working Capital Foundations: Measurement of Efficiency

by CTM News Team

After covering the two main formulas and definitions of working capital (accounting and treasury), which focused on a value or dollar amount, we now turn to working capital efficiency. This is a shift from dollars to days. Using a number of days as a metric provides finance teams with a way to track efficiency that won’t be skewed as a company grows.

It is important to understand the purpose of a formula in order to use it correctly. Managing liquidity certainly has an element of value or cash at every point in time. As a company expands in size or into new geographies, the demand on the cash will naturally shift. The change will either be managed purposefully, or it will simply be reported. All great treasurers manage working capital intentionally and formally.

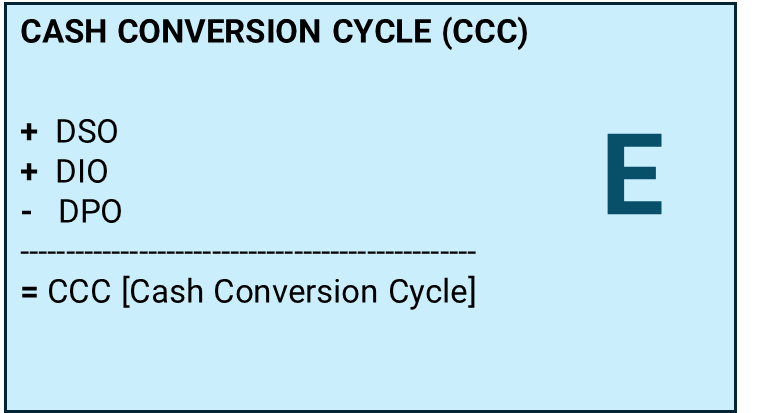

Cash Conversion Cycle (CCC) Formula

The CCC formula is shown below and is expressed as a number of days.

- Days sales outstanding (DSO)

- Days inventory outstanding (DIO)

- Days payables outstanding (DPO)

- Cash conversion cycle (CCC), a cycle-time of days

This reflects the total number of days of sales and inventory your company is holding. This is reduced by the number of days you hold onto your payables before settling with your vendors. Be aware that the days this formula measures are not equivalent to a dollar value. We will show why that is the case later.

DSO, DIO, DPO

Looking at the days.

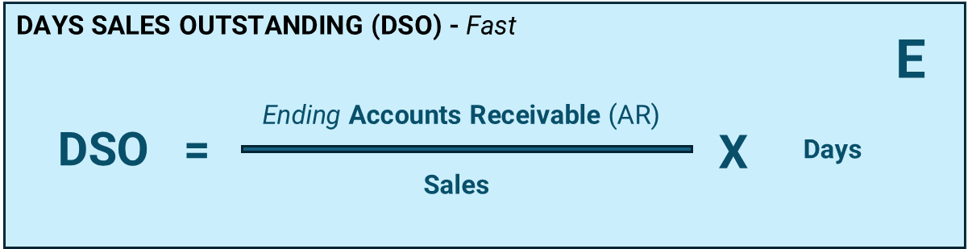

Receivables

DSO is the time it takes to convert receivables into cash on average. We start with a simple chart, which is the easiest to capture and calculate.

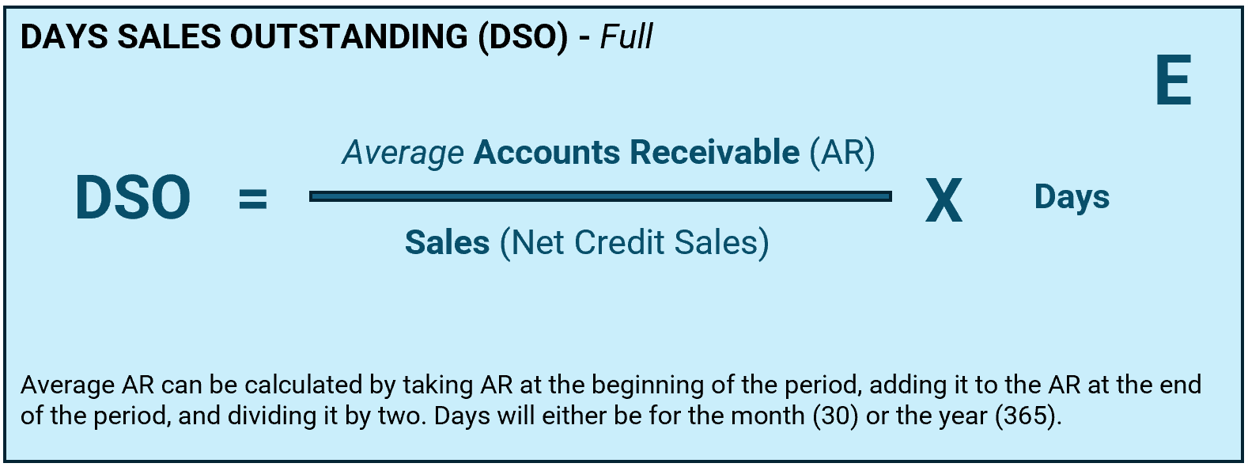

Note that we are using the ending AR balances instead of the average. This is usually a good proxy for reality, although using the average AR for the period is an improvement and is recommended. The more robust formula is:

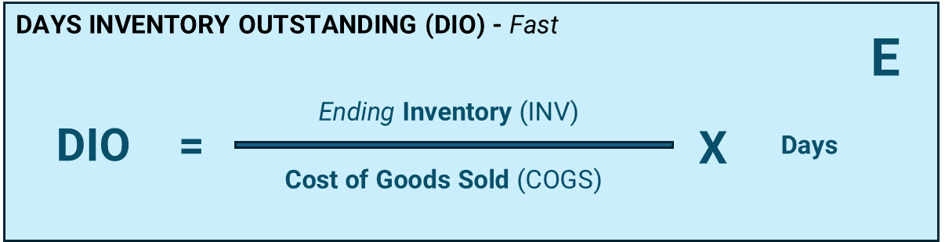

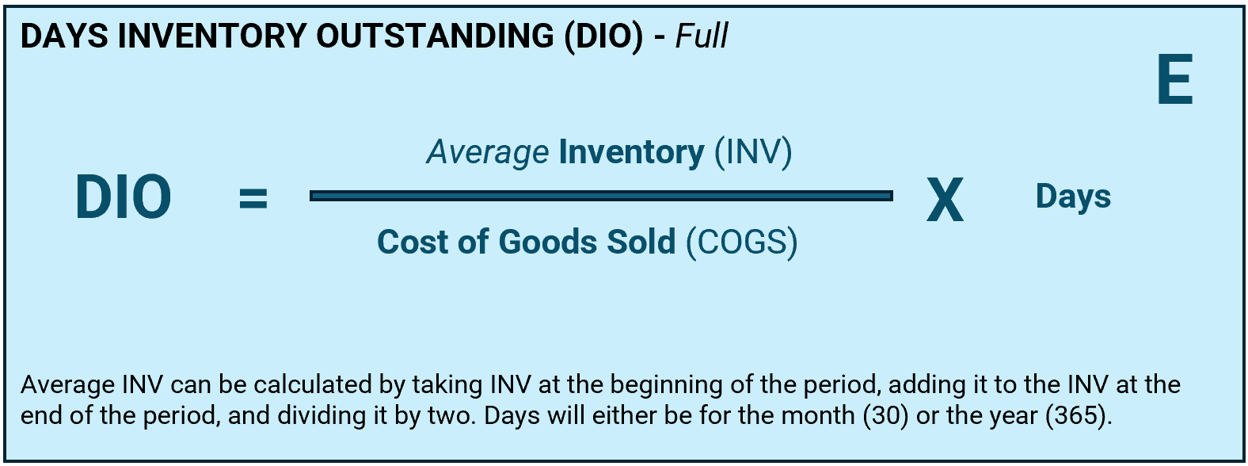

Inventory

DIO is the time you hold inventory before it is sold. We again start with the simple chart that is the easiest to capture and calculate.

The more detailed formula averages your inventory and is shown as:

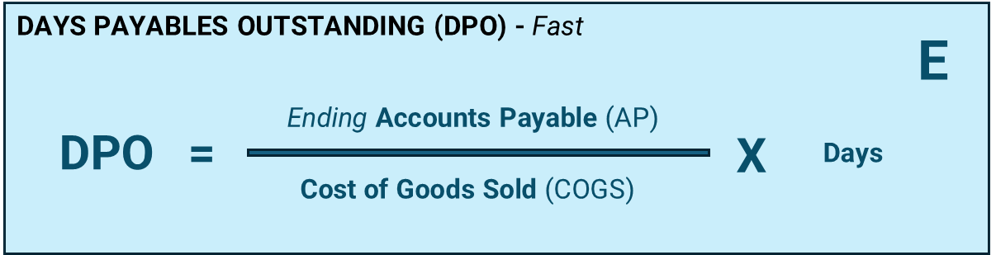

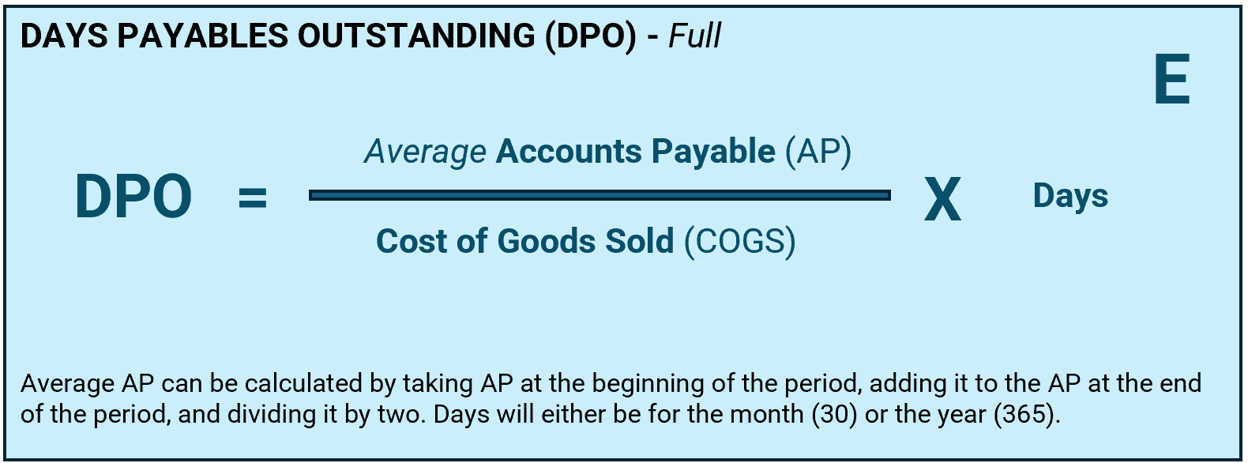

Payables

DPO is the time you hold invoices before paying your suppliers. Again, we begin with the simplified formula:

The more comprehensive formula:

Additional Thoughts on the CCC Formulas

Your overall efficiency is measured in days. Improved collection and inventory and optimized payables processes allow your organization can scale effectively, meaning that an increase or change in sales activity will not negatively impact the days used in any category.

Even if your organization’s sales remain constant, working on your efficiency translates into improved financial results. An example might be reducing your DSO by two days by working on invoicing accuracy, speed of delivery, and methods. These days translate into dollars that don’t need to be tied up in the cycle.

In a later article in this series, we will examine how creating a working capital council can focus attention on these processes and improve a company’s financial results.

Denominators and Days

If you look at all three formulas, you will notice one denominator is based upon sales (DSO), while two use cost of goods sold. Since we are looking at days as a calculation, we must use the measurements that fit with the numerator. DSO uses sales in the denominator since this is reflective of the receivables that are generated to make those sales. To illustrate with actual numbers, let’s assume sales of $36.5mm. This averages out to $100K per day. If you have an average $4mm of AR, that is the equivalent of 40 days of sales.

- $4,000,000 divided by $36,500,000 x 365 = 40 days.

- $4mm is the average AR.

- $36.5mm is the sales for the year.

- $4mm divided by $36.5mm represents the proportion of AR to sales (11%), about one-ninth of a year. One-twelfth of a year would be a month or about 30 days, so this represents more than 30 days.

- By multiplying this amount by 365, we convert that proportion to days. In this case, it is 40 days.

Efficiency measures all components in terms of days and is a great way of capturing how you make improvements in the CCC. Remember, though, that a day of DSO represents more capital, since (at least in healthy companies) sales exceeds the cost of those sales (COGS). Keep this difference in mind when you are converting days and improvements in the CCC to the capital required to support acquisitions or growth.

In the next article in this series, we will examine the process of improving an organization’s performance through a working capital council.

Like this item? Get our Weekly Update newsletter. Subscribe today